- Start with the market-entry objective

- Compare the regulatory maps, not just the labels

- Identify whether the product moves money or stores value

- Compare partner dependency before comparing speed

- Compare thresholds, capital, and scale assumptions

- Compare product complexity early

- Compare governance readiness

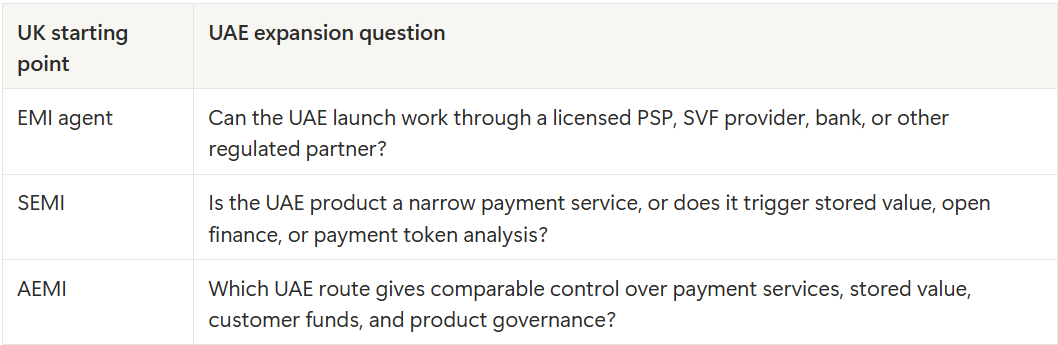

- UK-to-UAE: what to compare before entering

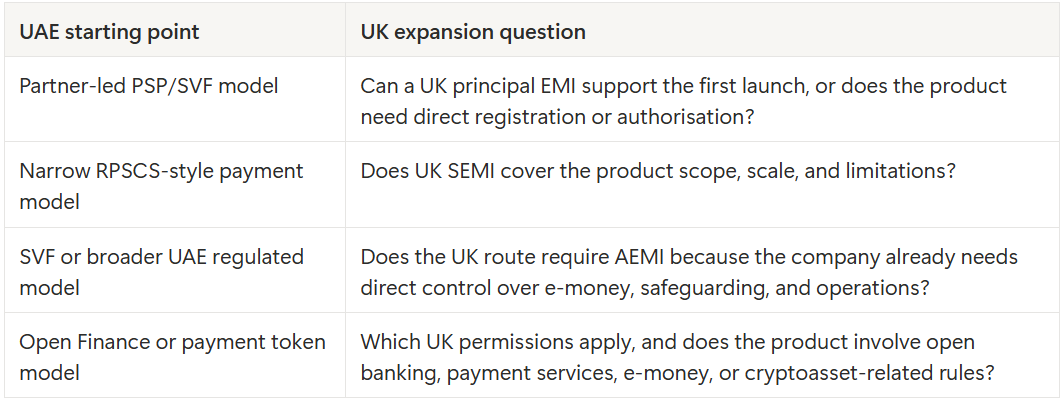

- UAE-to-UK: what to compare before entering

- Build a migration plan before the first launch

- Practical founder checklist

- Conclusion

A fintech that works in the UK does not automatically have a launch route for the UAE. The reverse is also true. A UAE fintech that understands local payment, wallet, or partner-led structures still needs to translate its operating model into the UK regulatory landscape before entering the market. The two markets can be compared, but they should not be treated as copies of each other.

The UK gives founders a relatively clear starting map around EMI agent, small EMI, and authorised EMI. The UAE uses a more product-based structure across retail payment services, stored value facilities, open finance, payment tokens, and partner-led arrangements with licensed entities. That difference changes the expansion question. Founders should not ask only, “Which licence do we need?” They should ask what the product does, who controls the regulated layer, where customer value sits, how much dependence the business can accept, and whether the next market is being tested or built as a long-term operating base.

At Finamp, we see UK vs UAE expansion as a business route comparison before we see it as a licensing exercise. The right route is shaped by product scope, launch speed, customer funds, partner dependency, governance maturity, and scale expectations. A company that compares those points early can avoid overbuilding too soon, entering through the wrong partner, or choosing a structure that blocks the product later.

Start with the market-entry objective

The first comparison is not legal. It is strategic.

A founder should define whether the next market is a validation market or a long-term regulated operating market. If the company is testing demand, local payment behaviour, onboarding assumptions, merchant appetite, support pressure, or corridor economics, a partner-led route may be enough for the first phase. If the company already knows the market is strategic and the product depends on direct control over balances, payment accounts, instruments, transfers, or regulated infrastructure, direct licensing may need to be assessed much earlier.

This logic applies in both directions. A UK fintech entering the UAE may start with a licensed PSP, SVF provider, bank, or another regulated partner if the use case is narrow and the partner can legally support it. A UAE fintech entering the UK may start through a principal EMI or sponsor-style structure if the goal is controlled market validation. In both cases, partner-first can reduce early friction. It can also create dependency that becomes expensive once the product starts to scale.

The founder’s first question should therefore be practical: are we entering this market to learn, or are we entering it to own the regulated operating model?

Compare the regulatory maps, not just the labels

The UK and UAE differ most clearly in how the initial route is framed. In the UK, the familiar EMI-related path is easier to explain. A company may launch through a principal EMI as an agent, consider small EMI status for limited UK independence, or pursue authorised EMI status when it is ready to carry broader governance, safeguarding, capital, and operational responsibility. The FCA states that firms need to be authorised or registered if they want to provide payment services or issue e-money, and its small EMI materials refer to the €5 million average outstanding e-money and €3 million monthly payment transaction thresholds used in the small EMI assessment. (FCA electronic money and payment institutions)

The UAE starts differently. The Central Bank of the UAE lists regulated areas such as Stored Value Facilities, Retail Payment Services, Card Scheme, and Open Finance. Its licensing materials describe Retail Payment Services through activities such as payment account issuance, payment instrument issuance, merchant acquiring, payment aggregation, domestic and cross-border fund transfer, payment token service, payment initiation, and payment account information service. (CBUAE Licensing)

This means founders should avoid looking for direct label equivalents. The UAE does not have a direct copy of the UK EMI agent / SEMI / AEMI ladder. It has routes that can serve similar business purposes, but the route depends on the product activity. A UK SEMI-like mental model may point toward a narrower UAE payment services category, but it will not solve a wallet or stored value product. A UK sponsor-model mindset may point toward a UAE partner-led structure, but the exact legal setup depends on the licensed partner’s permissions and the product’s regulated function.

Identify whether the product moves money or stores value

The stored value question is one of the most important differences between the two markets. A product that only moves funds in transit may be assessed differently from a product that lets users hold value for later use. In the UAE, this distinction can move the product from a retail payment services discussion into the Stored Value Facilities framework.

The CBUAE describes a Stored Value Facility as a facility where a customer, or another person on the customer’s behalf, pays money or money’s worth to the issuer in exchange for storage of that value and a relevant undertaking. The CBUAE licensing page also notes that SVF includes device-based and non-device-based stored value facilities. (CBUAE Licensing) (centralbank.ae)

This matters because SVF regulation is materially heavier than a narrow payment services route. The CBUAE rulebook states that SVF providers must maintain paid-up capital of at least AED 15 million, and the search result for the official SVF regulation also confirms that the framework covers licensing and ongoing supervision for companies providing SVF in the UAE. (CBUAE Stored Value Facilities Regulation)

For a UK fintech entering the UAE, this is a key translation point. A product that would be described in the UK through e-money logic may need to be mapped in the UAE through SVF analysis. For a UAE fintech entering the UK, the reverse question appears: does the existing wallet or stored value product require EMI status, and is the UK route better suited to an agent model, SEMI, or AEMI?

Compare partner dependency before comparing speed

Partner-first strategies can work well in both markets, but founders should compare the dependency, not only the speed.

In the UK, the EMI agent model can help a fintech launch faster because the principal EMI already holds the regulated status. The trade-off is that the principal remains responsible for the agent and must oversee it. The FCA’s small EMI application page states that a small EMI is responsible for anything done or omitted by its agents and should have appropriate systems and controls to oversee them effectively. (FCA small EMI application guidance)

In the UAE, a partner-led route may involve a licensed PSP, SVF provider, bank, or another regulated entity. The business effect can look similar to a sponsor route: faster entry, less direct regulatory burden at the beginning, and dependence on the licensed entity’s permissions, controls, risk appetite, and commercial terms. The legal structure is still UAE-specific and should be tied to the actual regulated activity, whether that is retail payment services, stored value, open finance, or payment tokens.

The right comparison is therefore not “Which market lets us launch faster?” The better comparison is “Which dependency can we live with during the first phase, and how hard will it be to migrate later?” A sponsor or partner model is often efficient while uncertainty is high. It becomes restrictive when every new feature, corridor, risk decision, customer segment, or pricing change depends on another company’s approval.

Compare thresholds, capital, and scale assumptions

Founders often compare licences by headline complexity, but the better comparison is scale fit.

In the UK, SEMI can work as a limited independence step, but it has hard limits. The FCA small EMI page says applicants must provide evidence that their e-money business will generate monthly average outstanding electronic money of less than €5 million and that monthly average payment services transactions did not exceed €3 million, based on the previous 12 months or projections where the firm has not traded. (FCA small EMI application guidance)

In the UAE, scale logic is tied to licence category, transaction value, and activity type. The RPSCS framework uses licence categories for different retail payment service scopes, while SVF introduces a separate and heavier capital profile for stored value. The CBUAE rulebook materials also show that retail payment services are divided into categories, with Category I, II, III, and IV licences depending on the services provided. (CBUAE RPSCS licence categories)

This creates a practical expansion question. If a UK fintech is small enough for SEMI, that does not mean it has found a lightweight UAE equivalent. If a UAE fintech operates under a narrower UAE route, that does not mean UK SEMI will cover the same roadmap. The founder must compare the expected transaction volume, customer float, regulated activities, and product roadmap in the target market rather than assume that a “small” route in one jurisdiction maps to a “small” route in the other.

Compare product complexity early

Product complexity often matters more than company size. A relatively small fintech can still require a more demanding route if the product combines several regulated functions.

In the UAE, a product may involve retail payment services, stored value, open finance, and payment tokens in different combinations. Open Finance is relevant where the product uses data sharing or service initiation. The CBUAE rulebook states that an Open Finance Provider must not receive, hold, or transfer funds for or on behalf of a user, which means Open Finance does not replace payment or stored value permissions. (CBUAE Open Finance limitations)

Payment tokens require a separate check. The CBUAE Payment Token Services Regulation lays down the rules and conditions for licensing or registration of Payment Token Services, and official rulebook materials describe payment token services as a regulated area. (CBUAE Payment Token Services Regulation)

For founders, the point is simple: a roadmap can outgrow a launch route before the business becomes large. A UK fintech entering the UAE may start with a straightforward payment feature but later add wallet balances, open finance data access, or token-based settlement. A UAE fintech entering the UK may start with a familiar product but discover that AIS, PIS, e-money issuance, safeguarding, or agent dependency changes the best route. Expansion planning should therefore compare the next two or three product phases, not just the first launch version.

Compare governance readiness

The move from partner-led entry to direct licensing is also a governance decision. A company that owns the regulated layer needs a stronger operating model than a company testing a product through a partner.

In the UK, direct EMI authorisation brings expectations around governance, internal procedures, responsible managers, safeguarding, and evidence of how the business will operate. The FCA’s pages on electronic money and payment institutions direct firms to authorisation, safeguarding, conduct, and approach materials as part of the regulated firm journey. (FCA electronic money and payment institutions) (FCA)

In the UAE, direct routes can require significant local substance, controls, capital, and supervisory engagement, especially where the product involves stored value, broader retail payment services, or payment tokens. Partner-first does not remove governance work, but it changes how responsibility is shared or controlled. Licence-first brings more of that responsibility into the company from the beginning.

The founder should ask whether the team is ready to operate as a regulated institution in the target market. That includes compliance leadership, risk controls, AML/CFT processes, customer support, incident response, reconciliation, safeguarding or float management, outsourcing oversight, reporting, and documentation. If the company is not ready, partner-first may be more practical. If the company is already building those functions and the product depends on direct control, licence-first may be more coherent.

UK-to-UAE: what to compare before entering

A UK fintech entering the UAE should translate its UK route into UAE business questions.

If the company operates as a UK EMI agent, the UAE comparison is not “find the same agent status.” The question is whether a licensed UAE partner can support the product and whether the partner’s permissions cover the regulated function. If the company is a UK SEMI, the UAE comparison is whether the product fits a narrower RPSCS route or whether stored value makes the SVF framework central. If the company is a UK AEMI, the UAE comparison is whether the same level of control requires direct CBUAE licensing, SVF licensing, Open Finance permissions, Payment Token Services permissions, or a combined route.

This comparison should happen before entity setup, partner negotiation, or product localisation. Otherwise, the company may build a UAE go-to-market plan around a structure that cannot support the product it wants to sell.

UAE-to-UK: what to compare before entering

A UAE fintech entering the UK should do the reverse translation.

If the company uses a UAE partner-led model, a UK principal EMI route may support initial market validation. If the company operates a narrow UAE payment service, SEMI may be worth assessing, but only if the UK product fits the thresholds and does not require AIS or PIS. If the company already owns a more complex UAE regulated layer, AEMI may need to be assessed earlier because the business may have outgrown the practical limits of a sponsor or small EMI route.

The UK may feel simpler because the EMI ladder is clearer, but that does not make the route automatic. A UAE product that already combines balances, payment instruments, cross-border payments, or data functionality may be too complex for a narrow UK entry structure.

Build a migration plan before the first launch

The most mature expansion strategies do not treat the first route as permanent. They define a launch route and a migration route together.

A partner-first launch should include a plan for what happens if the market works. That means understanding data portability, customer communication, ledger or transaction record migration, contractual exit rights, settlement continuity, compliance responsibility, and the point at which direct licensing becomes more efficient. Without that plan, the company may succeed commercially and then discover that the operating model cannot scale without painful restructuring.

A licence-first launch should include a different kind of discipline. The company should know why direct licensing is needed now, not simply why it might be useful someday. Direct licensing should be tied to product control, customer funds, economics, governance, partner requirements, or long-term market commitment. Otherwise, the company may spend too much time and capital before proving the target market.

This is where Finamp’s view is deliberately practical. Expansion is not about choosing the most impressive regulatory route. It is about choosing the route that matches the next stage of the business and still leaves room for the stage after that.

Practical founder checklist

Before expanding from the UK to the UAE, or from the UAE to the UK, founders should compare the following points:

- Does the product only move funds, or does it store value?

- Which regulated activities does the product perform in the target market?

- Can the first version launch through a licensed partner without blocking the roadmap?

- Which party controls customer funds, compliance decisions, reconciliation, and customer communications?

- Does the product involve payment accounts, instruments, merchant acquiring, aggregation, domestic transfers, or cross-border transfers?

- Does the product involve account information, payment initiation, open finance, or service initiation?

- Does the product involve payment tokens or stablecoin-like settlement?

- What are the expected transaction volume, customer float, and growth path over the first 12 to 24 months?

- What level of governance, compliance, and operational substance is the company ready to carry now?

- What will trigger a move from partner-led entry to direct licensing?

This checklist is intentionally business-focused. It helps the founder avoid starting with labels and then forcing the product into them.

Conclusion

UK and UAE fintech launch routes can be compared usefully, but only when founders compare the right things. The UK route is clearer as a staged EMI model: agent, small EMI, authorised EMI. The UAE route is more product-based: retail payment services, stored value, open finance, payment tokens, free-zone context, and partner-led structures.

The best expansion planning starts with the product and the market-entry objective. If the goal is learning, a partner-first model may be the right first move. If the goal is long-term regulated ownership, direct licensing may need to start earlier. If the product stores value, uses payment tokens, or combines multiple regulated functions, the route becomes more complex and should be mapped before the company makes commercial commitments.

Founders should compare speed, control, dependency, capital, product scope, governance, and migration risk before choosing a launch route. That is the difference between entering a new market quickly and entering it with a structure that can still support the business after the first version works.