- The core idea: choose a stack that reduces dependencies, not one that adds them

- Three questions that unblock partner selection quickly

- Quick definitions in plain English

- What each option solves and what it does not

- The key timeline unlock: what you can postpone safely and what you cannot

- Typical partner stacks and when each makes sense

- The partner selection scorecard (criteria, red flags, timeline impact)

- The sequencing playbook that prevents partner-driven stalls

- Where Finamp fits (and how it helps you choose partners without pausing delivery)

Most neobank founders do not get stuck because the product idea is unclear. They get stuck because partner selection quietly turns into a dependency chain. One “quick call” becomes five. Each partner introduces new requirements. Timelines slip, and the MVP becomes a procurement project.

This page is a practical way out. It explains what BaaS, EMI, and BIN sponsorship actually do in a neobank stack, how each choice affects build timelines, and which decisions unblock delivery without locking you into the wrong operating model. It is written for founders who are searching “how do I choose partners” and “what decisions unblock build timelines.”

One framing to keep in mind throughout: regulated partners do not approve roadmaps. They approve evidence. If your MVP cannot produce evidence of control, money movement behaviour, and operational handling, the stack choice will not save you. It will only delay the moment you discover what you are missing.

The core idea: choose a stack that reduces dependencies, not one that adds them

A partner stack is not a single decision. It is a sequence of decisions across three layers:

- Regulated connectivity: how accounts, payments, and settlement are enabled (and who is legally responsible).

- Card scheme access (if cards are in scope): how you issue and operate a card program and under whose scheme membership.

- The product and operations layer: how the system behaves over time, including transaction states, audit events, support, disputes, complaints, monitoring, and governance.

Most timeline stalls happen when founders treat regulated connectivity and cards as “the real work” and treat the product and operations layer as “later.” In practice, the product and operations layer is what makes partner conversations move faster, because it lets you answer the questions that trigger delays: “What happens when this fails?”, “Who can do what?”, “Where is the evidence?”

The fastest teams do not “finalise partners” before building. They build an evidence-capable core while partner selection is still in motion, so delivery does not pause waiting for external decisions.

Three questions that unblock partner selection quickly

Before comparing vendors or licensing routes, answer these three questions in plain English. You do not need perfect legal phrasing, you need clarity that prevents accidental scope expansion.

1) Are you holding customer funds at MVP launch, or validating with demo or sandbox flows first?

If you are not holding funds yet, you can move faster. But you still need a transaction lifecycle model and audit events so the demo is not throwaway work.

2) Are cards truly in Day 1 scope, or are they phase two?

Cards pull BIN sponsorship and scheme program requirements into your critical path. If cards are not Day 1, keep the architecture card-ready without making sponsorship approval the thing that blocks your MVP.

3) What is your Day 1 geography and regulatory path?

Even when “licensing is handled by partners,” markets drive real requirements: disclosures, consent, data governance expectations, rail behaviour, and operational processes.

If these three answers are fuzzy, partner conversations will add requirements faster than you can validate them, and your build plan will keep changing mid-flight.

Quick definitions in plain English

What BaaS usually means

Banking-as-a-Service usually means a regulated provider that exposes banking capabilities through APIs, such as accounts and payments, and sometimes cards depending on the model. BaaS gives you rails and regulated connectivity. It does not automatically give you the full product layer: apps, support tooling, operational workflows, and the evidence trail that partners will ask for.

What EMI means

An Electronic Money Institution is a regulated entity authorised to issue electronic money and provide certain payment services (scope varies by jurisdiction). In the UK, the framework is set out in the Electronic Money Regulations 2011. (legislation.gov.uk) In the EU, Directive 2009/110/EC establishes the regime for electronic money institutions. (EUR-Lex)

Founders often use “EMI” as shorthand for “a regulated umbrella that can shorten time-to-live compared to becoming a bank,” but it is not a shortcut around operational readiness or evidence.

What BIN sponsor means

A BIN sponsor is a scheme member (or principal client) that sponsors your card program under their scheme relationship. In Visa’s licensing model, associate clients can operate with the sponsorship of a principal client, with the principal supporting scheme obligations such as settlement and reporting. (Visa Partner)

In other words, BIN sponsorship is not just access. It is an operating model where a sponsor carries responsibilities, and your program must be designed to meet the sponsor’s oversight expectations.

What each option solves and what it does not

BaaS: regulated rails and account connectivity

BaaS is the layer that turns “transfer money” from a UI concept into a real service. It is where domestic rails, settlement states, reconciliation, and failure behaviours live.

Where founders get surprised is that integration is rarely one task. Even for a narrow MVP, you end up designing product decisions around rail behaviour: pending states, returns, cutoffs, retries, and the difference between “we initiated it” and “it settled.”

If you choose a BaaS path, your build stays fast when you do two things early:

- Define your transaction lifecycle model inside your product core. Your states become your stable language (initiated, pending, completed, failed, reversed, refunded). Later, you map each partner’s events into this model instead of rewriting product logic for every provider’s quirks.

- Build the operational layer that makes rails survivable. Status visibility, customer notifications, internal monitoring, and support scripts tied to real failure states.

A useful UK example of why this matters: the Faster Payment System supports near real-time payments and runs 24/7/365. (Pay.UK) If a UK-facing product is vague about payment states, users interpret delay as risk. Partners interpret it as operational immaturity.

EMI: a regulated umbrella for issuing e-money and delivering payment services

An EMI route matters when your model depends on issuing e-money and operating under a structured payment services framework, or when you want a regulated entity to carry specific regulatory responsibilities while you build and distribute the product.

The UK and EU EMI frameworks are established and commonly referenced in partner conversations. (legislation.gov.uk, EUR-Lex)

The common mistake is assuming that working with an EMI removes the need for evidence. In reality, it changes what evidence is expected and who asks for it. An EMI will still assess whether your product can enforce controls, record outcomes, manage customer issues, and demonstrate oversight.

If your MVP cannot show how the system behaves over time, you still stall. You just stall later, when changing direction is more expensive.

BIN sponsor: scheme access for cards and a sponsor-led operating model

If cards are in your Day 1 scope, BIN sponsorship can become your true gate. The sponsor is not simply enabling card issuance. They are taking scheme and risk obligations seriously, and they will evaluate your readiness accordingly. Visa’s own licensing materials describe sponsorship structures where the principal client supports associate clients on scheme obligations. (Visa Partner)

A card program creates operational realities that many MVPs ignore until it is too late, including disputes, reversals, chargebacks, fraud handling, and support load.

Sponsors tend to slow down when they see “feature thinking” (virtual card, freeze/unfreeze). They move faster when they see “operating model thinking,” including:

- a coherent transaction lifecycle that covers card events and outcomes,

- structured handling for disputes and chargebacks,

- escalation paths and monitoring,

- evidence trails for key actions and changes.

If your MVP is card-led, make that explicit and treat sponsorship as an early workstream. If it is not card-led, keep the architecture card-ready while avoiding sponsorship approval as a Day 1 dependency.

The key timeline unlock: what you can postpone safely and what you cannot

Many teams try to finalise everything early because it feels safer. In practice, that is how they stall.

You can often postpone final vendor selection, commercial negotiation, and some scheme-specific details without blocking meaningful MVP progress, as long as your core is built correctly.

What you cannot postpone is the evidence layer and the operating model. Without those, every partner conversation produces new requirements that become rebuild work.

This principle shows up clearly in outsourcing and operational resilience expectations. The FCA’s guidance on outsourcing to the cloud and other third-party IT services emphasises oversight, risk management, access, and control across third parties. (FCA) Even outside the UK, partner due diligence tends to follow similar patterns.

A simple rule helps: if changing something would require sign-off from compliance, legal, a sponsor bank, or a scheme partner, it should be designed as configuration and evidence, not hardcoded logic.

Typical partner stacks and when each makes sense

Stack 1: Evidence-first MVP, partner integrations staged later

This is often the fastest path for investor validation and controlled MVP delivery. You build a credible product core first, then connect production rails once the partner path is clear.

A sensible Stage 1 scope usually includes:

- onboarding flows with configurable KYC steps,

- transaction lifecycle modelling (money movement can be simulated at this stage),

- admin tooling and audit events,

- operational workflows for support and complaints.

This avoids the “demo that cannot become production” trap because the foundations are real, only the connectivity layer changes.

Stack 2: BaaS-first MVP, real money movement early

This can be the right choice when the business model requires real funding and transfers early. The risk is dependency creep: integration expands scope, testing takes longer than expected, and you start building around a partner’s edge cases without a stable internal model.

If you go BaaS-first, protect the timeline by locking scope, defining your transaction lifecycle model early, and building operational handling in parallel.

Stack 3: EMI-led go-live path

This stack is common when your model aligns strongly with e-money issuance and regulated payment services from day one. The benefit is reduced ambiguity around safeguarding and governance. (legislation.gov.uk, EUR-Lex)

The risk is over-solving licensing early and freezing delivery while you negotiate details that do not need to block the MVP build. The build stays fast when licensing informs product boundaries, but does not stop the product layer from progressing.

Stack 4: Card-first MVP with BIN sponsorship on the critical path

This is viable when your product is truly card-led and you have a sponsor path that matches your risk profile. Visa’s model explicitly frames sponsorship structures for programs. (Visa Partner)

Treat this as a program launch, not a UI launch. Your speed depends on demonstrating operational readiness, dispute handling, and evidence trails early.

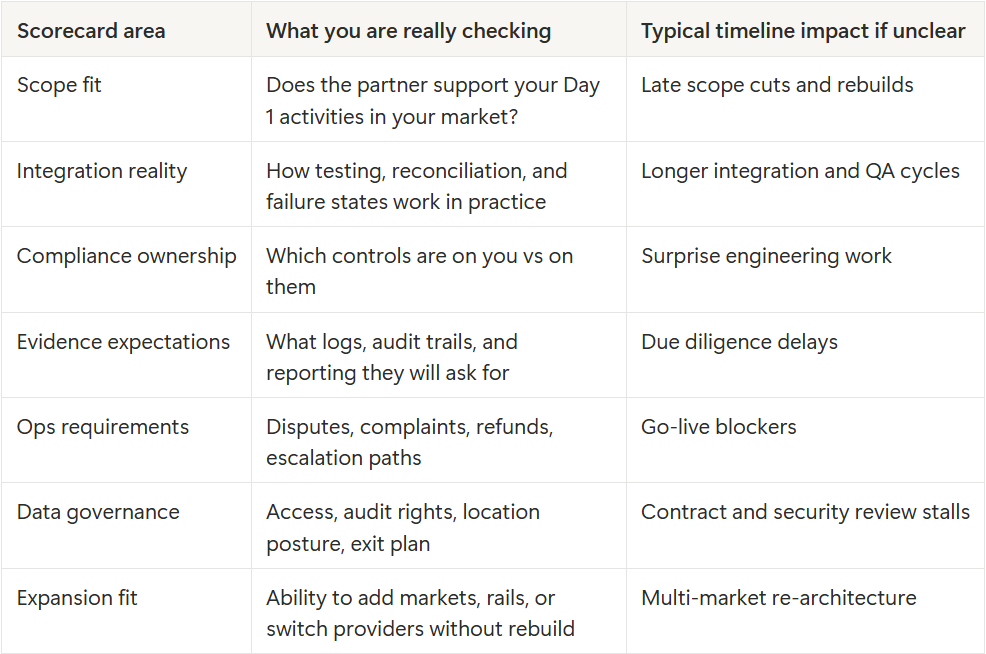

The partner selection scorecard (criteria, red flags, timeline impact)

The goal of a scorecard is not to pick “the best” partner on paper. It is to predict where you will lose time, and whether that time loss is avoidable.

Criteria that most strongly affect build timelines

Use these to compare options consistently, even when vendors market themselves differently.

Red flags that predict delay

Delay rarely comes from one big problem. It usually comes from several “unknowns” that stack up. Consider these as warning signs that your timeline will slip unless you adjust scope or sequencing.

- The partner cannot clearly describe failure behaviour and settlement states.

- A sandbox or realistic testing environment is vague or unavailable.

- Due diligence evidence requirements are not concrete.

- Exit, portability, or data access rights are “we can discuss later.”

- Pricing logic is embedded inside payment routing in a way that forces code changes for every change request.

- For cards, the sponsor expects mature dispute handling, but your operating model is not designed yet.

A simple timeline rating

For each option, assign three ratings: build dependency risk, compliance dependency risk, and operational maturity requirement (Low, Medium, High). If any category is High, it does not mean you should not proceed. It means you should avoid making that choice the blocker for building the product core.

The sequencing playbook that prevents partner-driven stalls

This is the practical sequence that keeps momentum even when partner selection is still in flight.

Step 1: Lock Day 1 scope in one page

Keep it simple and explicit: money actions, whether cards exist, which market you start in, and whether funds are real or simulated. This prevents partner calls from expanding scope by accident.

Step 2: Define your transaction lifecycle model before touching rails

A stable lifecycle model is a major accelerator because it prevents rebuilds. Your goal is to have one internal language for outcomes and evidence, then map partner events into it.

A minimal lifecycle usually includes:

- clear states (initiated, pending, completed, failed, reversed, refunded),

- reason codes for failures,

- customer notification triggers,

- reconciliation hooks and “finality” expectations.

Step 3: Build the evidence layer alongside the MVP

This is where “ready” becomes provable. At MVP stage, focus on evidence that partners consistently ask for:

- audit-friendly event trails for risk-relevant actions,

- admin action logging and permissioning,

- disclosure and consent versioning,

- structured records for support, complaints, and outcomes.

In Open Banking contexts, consent is a lifecycle rather than a one-off screen, and re-authentication dynamics affect retention and support load. The Open Banking standards body documents the impact of 90-day re-authentication on user experience and drop-off. (Open Banking) The broader lesson applies to most regulated experiences: lifecycle events must be visible, explainable, and auditable.

Step 4: Use evidence questions in partner calls

Feature checklists are easy to sell and hard to operate. Evidence questions surface the real blockers early.

Ask:

- What evidence will you require during due diligence?

- What operational workflows must exist at launch (complaints, disputes, refunds)?

- What are your expectations for outsourcing oversight and audit access?

- What are the most common launch failure modes, and how should we handle them?

UK guidance on outsourcing and oversight is a good reference point for the type of questions that appear in regulated ecosystems. (FCA)

Step 5: Keep country and partner differences as configuration

If you plan multi-market expansion, avoid hardcoding onboarding rules, disclosures, eligibility constraints, and corridor availability. When these become code changes, every new market becomes a rebuild.

Where Finamp fits (and how it helps you choose partners without pausing delivery)

Finamp is designed for the exact problem described in this article: choosing the right partner stack without turning the build into a dependency chain.

Finamp sits as a product layer above regulated connectivity. That means you can build the parts that partners and regulators actually scrutinise early, while partner selection and contracting runs in parallel. Teams use Finamp to:

- build audit-friendly event trails so proof is a natural output of the system,

- implement transaction lifecycles with traceable states and outcomes, so partner behaviours map cleanly into a stable internal model,

- ship operational foundations early, including admin controls and workflows for complaints and dispute handling,

- stay flexible across markets by keeping country-level differences configurable rather than embedded in the product core.

This aligns with the staged delivery logic used across the Finamp content system: prove quickly without throwaway work, then connect the right partners and go live without rebuilding.

If you want a fast sanity check on your partner stack, Finamp teams can map which decisions must be made now, which can safely wait, and what evidence your next partner will expect to see.

Book a call with Finamp to pressure-test your stack and keep your build timeline credible.