- In the UK, sponsor dependency is easier to describe

- In the UAE, sponsor dependency is more product-specific

- The UAE adds stored value dependency

- Outsourcing and operational control matter more than the label

- Dependency is shaped by what the product must control

- The economics of dependency also differ

- Migration risk should be designed early

- Partner-first is still often the right first move

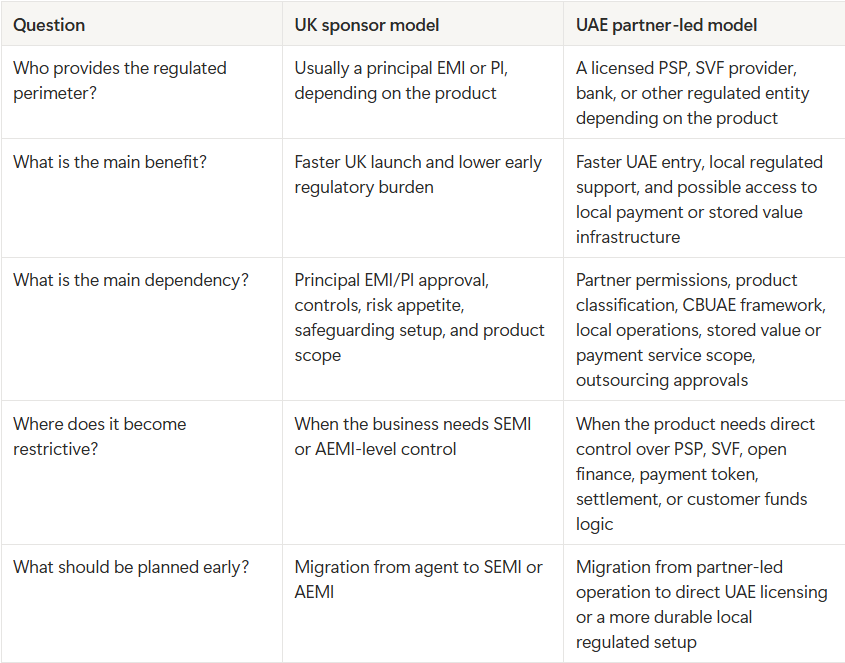

- Practical comparison for founders

- What founders should decide before signing with a sponsor or partner

- Conclusion

Sponsor dependency is one of the most important trade-offs in fintech market entry. It can help a company launch faster, reduce early regulatory burden, and test demand before building a regulated institution in its own name. It can also slow product changes, compress margins, limit roadmap flexibility, and create migration risk once the business starts to scale.

The UK and the UAE both allow fintechs to work through licensed entities in different ways, but the dependency does not look the same in each market. In the UK, sponsor dependency is often discussed through the familiar EMI agent model: a fintech operates through a principal EMI, and the principal carries regulatory responsibility for the agent. In the UAE, the same business idea can appear through a licensed PSP, SVF provider, bank, agent, outsourcing arrangement, or another regulated partner, depending on what the product actually does.

At Finamp, we treat sponsor dependency as a business-model question before we treat it as a legal detail. The right question is not only whether a partner can support the launch. The more important question is what the fintech becomes dependent on: the licence, the product scope, customer funds infrastructure, transaction monitoring, local operations, settlement, data access, payment tokens, or future migration path. That is where the UK and UAE start to diverge.

In the UK, sponsor dependency is easier to describe

The UK model gives founders a relatively clear starting point. If a fintech does not want to become an EMI immediately, it may launch through a principal EMI as an agent. The FCA describes an agent as a person acting on behalf of a PI, EMI, or RAISP in the provision of payment services. The FCA also states that PIs, EMIs, and RAISPs are responsible for anything done or omitted by their agents, and it expects them to have appropriate systems and controls to oversee agents effectively. (FCA Payment Services and Electronic Money Approach Document)

That creates a clean commercial pattern. The startup gets access to a regulated perimeter without carrying the full burden of direct authorisation. The principal EMI gets responsibility and therefore control. The founder gains speed, but accepts oversight, approval layers, risk appetite limits, commercial fees, and dependence on the principal’s infrastructure and interpretation of the product.

There is also a clear ceiling. The FCA states that an EMI may distribute or redeem e-money through an agent or distributor, but may not issue e-money through an agent or distributor. This matters because it shows that the startup can operate through the model, but it does not fully own the regulated e-money layer. The dependency is built into the structure. (FCA Payment Services and Electronic Money Approach Document)

For founders, this makes the UK sponsor conversation relatively easy to frame. The EMI agent route is useful when the business needs speed and market learning. SEMI may become relevant when the company wants limited UK independence. AEMI becomes relevant when sponsor dependence becomes too expensive or restrictive for the product, governance model, and economics.

In the UAE, sponsor dependency is more product-specific

The UAE does not have a direct copy of the UK EMI agent / SEMI / AEMI ladder. A sponsor-like route may exist in business terms, but its shape depends on whether the product is a retail payment service, stored value facility, open finance service, payment token service, card-related product, or a combination of those functions.

The Central Bank of the UAE’s Retail Payment Services and Card Schemes Regulation covers digital payment services such as payment account issuance, payment instrument issuance, merchant acquiring, payment aggregation, domestic and cross-border fund transfer, payment token services, payment initiation, and payment account information services. This means a fintech has to classify the product before it can understand what kind of licensed partner may support it. (CBUAE Retail Payment Services and Card Schemes Regulation)

The UAE framework also recognises agents and branches under the retail payment services regime. If a Payment Service Provider intends to provide Retail Payment Services through an agent or branch, it must assess the arrangement and report annually to the Central Bank on points such as the agent’s name and address, internal controls for AML/CFT, fit and proper assessment of responsible persons, and the scope of services mandated to the agent. PSPs must also contractually ensure that agents disclose that they act on the PSP’s behalf. (CBUAE Retail Payment Services and Card Schemes Regulation)

This gives founders a partner-led route, but the structure is not the same as simply becoming a UK-style EMI agent. A UAE sponsor-like arrangement may be narrower, broader, or more complex depending on the licensed partner’s permissions and the product’s regulated function. A payment aggregation product, wallet, cross-border transfer product, open finance service, and payment token product can all create different dependency patterns.

The UAE adds stored value dependency

Stored value is one of the biggest reasons sponsor dependency looks different in the UAE. A fintech that stores customer value, operates a wallet, or allows users to hold value for future payments may need to assess the Stored Value Facilities framework rather than only the Retail Payment Services framework.

Under the UAE Stored Value Facilities Regulation, an SVF licensee is responsible for the acts or omissions of its employees, service providers, and agents in respect of the conduct of its business. The regulation also states that employees and agents of a licensee must be properly trained and qualified. (CBUAE SVF Regulation)

This changes the dependency question. If the product depends on stored balances, customer float, vouchers, wallet value, reward value, or prepaid functionality, the fintech may become dependent on a licensed SVF provider rather than a general payment sponsor. That dependency can reach deeper into the product because stored value affects ledger design, float management, reconciliation, redemption, customer terms, and operational controls.

In the UK, a sponsor discussion often starts with the principal EMI and the agent model. In the UAE, a wallet founder may need to ask a more specific question: who controls the stored value layer, who is responsible for the float, who manages redemption, and how much of the wallet logic can the fintech actually own while operating through a partner?

Outsourcing and operational control matter more than the label

Sponsor dependency is not only about the licensed entity. It is also about outsourced operations, service providers, technical infrastructure, and who controls the real operating chain behind the product.

The UAE RPSCS Regulation states that PSPs outsourcing services and processes to service providers, agents, or group entities must contractually ensure that those third parties comply with the regulation, Level 2 Acts, and other relevant laws. It also states that outsourcing is subject to prior Central Bank approval, and that PSPs must provide annual reports on outsourcing arrangements. PSPs remain fully liable for acts of any agent, branch, or service provider to which a Retail Payment Service has been outsourced. (CBUAE Retail Payment Services and Card Schemes Regulation)

The SVF framework takes a similar direction. An SVF licensee may outsource activities and processes to service providers, but outsourcing must be approved by the Central Bank. The licensee remains ultimately responsible for the adequacy, service levels, quality, security, reliability, robustness, stability, and availability of outsourced activities and processes. (CBUAE SVF Regulation)

For founders, this means the UAE partner-first model should be reviewed as an operating architecture, not just a commercial shortcut. The fintech may depend on a licensed partner, but it may also depend on that partner’s service providers, banking relationships, outsourcing approvals, technology standards, operational procedures, and reporting obligations. The more operational layers sit outside the fintech’s control, the more important it becomes to understand service levels, data rights, migration rights, customer communication responsibilities, and control ownership from the beginning.

Dependency is shaped by what the product must control

In both markets, sponsor dependency becomes restrictive when the fintech needs more control than the partner model can provide. The difference is where that control pressure usually appears.

In the UK, the pressure often appears around product roadmap, principal approval, safeguarding design, e-money issuance, payment services scope, and the decision to move toward SEMI or AEMI. The founder can usually frame the next step through the UK EMI sequence: stay under the principal, move to small EMI if the product is limited enough, or pursue authorised EMI when the business needs fuller control.

In the UAE, the pressure may appear around a more fragmented set of control points. A fintech may need direct control over the PSP licence scope, stored value facility, merchant acquiring setup, payment aggregation model, cross-border transfer flow, payment account structure, open finance access, payment token functionality, or local operational substance. The next step is not a single ladder. It is a product-specific licensing and operating decision.

This makes UAE dependency more sensitive to product design. A company can start partner-first for a narrow use case and still be in a good position. But if the product roadmap already depends on stored value, payment tokens, or multiple regulated payment services, the partner model may become restrictive faster than expected.

The economics of dependency also differ

Sponsor dependency has direct economic consequences in both markets. The fintech may pay setup fees, monthly fees, revenue share, transaction fees, compliance review costs, integration costs, or migration costs. It may also lose margin indirectly through slower approvals, limited product flexibility, partner-controlled pricing, or operational constraints.

In the UK, these costs are usually assessed against the alternative routes of SEMI or AEMI. If the company is still validating demand, sponsor cost may be acceptable. If the product is scaling and dependence is now reducing margin or slowing roadmap execution, direct authorisation starts to become more attractive.

In the UAE, the economic comparison can be less linear. A partner-first route may avoid direct licensing and capital burden at first, but the alternative may not be a small EMI-style middle step. If the product stores value, the direct route may involve SVF licensing and significantly heavier capital and float requirements. If the product sits under RPSCS, the direct route depends on the category and transaction scale. If the product involves open finance or payment tokens, a separate route may be needed.

That means UAE sponsor dependency can remain economically attractive for longer in some cases, especially for early validation. In other cases, it can become expensive quickly because the partner controls the most valuable part of the product: wallet balances, settlement access, merchant acceptance, local payment operations, or token functionality.

Migration risk should be designed early

The most dangerous form of sponsor dependency is not the initial dependency. It is dependency without an exit plan.

A UK fintech operating through a principal EMI should know what will happen if it later moves to SEMI or AEMI. That includes customer communications, contractual rights, data portability, transaction history, safeguarding arrangements, complaint handling, operational continuity, and technical migration. A founder should avoid building the whole UK operating model around a principal without understanding how the business would separate if market traction justifies direct registration or authorisation.

The same logic applies in the UAE, but the migration can be more complex. If the fintech starts through a licensed PSP or SVF provider, moving later to direct licensing may require changes to customer terms, wallet records, float arrangements, bank accounts, merchant agreements, settlement flows, outsourcing arrangements, and possibly the regulated activity mix. If payment tokens or open finance are involved, the migration plan may need to account for additional permissions and partner dependencies.

This is why the first partner agreement should be written with the second phase in mind. The founder should understand who owns the customer relationship, who controls the data, how records can be exported, how balances can be transferred or redeemed, what happens to live transactions, and what operational support the partner must provide during migration.

Partner-first is still often the right first move

None of this means sponsor dependency is bad. For many fintechs, partner-first is the most sensible route into a new market.

In the UK, a principal EMI can help a company test demand before committing to SEMI or AEMI. In the UAE, a licensed PSP, SVF provider, bank, or other regulated partner can help a company test local demand before carrying a heavier licensing and operating burden. This is especially valuable when the company is still learning local onboarding expectations, payment preferences, merchant behaviour, support pressure, transaction patterns, fraud exposure, and unit economics.

The point is to use dependency deliberately. A partner-first route is strongest when it gives the company speed and learning while preserving future options. It becomes weaker when the product quietly becomes dependent on infrastructure the fintech will eventually need to control.

Practical comparison for founders

The easiest way to compare sponsor dependency in the UK and UAE is to ask what the company depends on.

The comparison shows why the same phrase, sponsor dependency, can mislead founders. In the UK, the dependency usually sits inside a clearer EMI sequence. In the UAE, it sits inside a product-specific regulatory and operating map.

What founders should decide before signing with a sponsor or partner

Before committing to a sponsor or partner-led structure, founders should answer several practical questions.

First, what regulated function is the partner actually supporting? In the UK, this may be e-money or payment services. In the UAE, it may be retail payment services, stored value, card-related activity, open finance, payment tokens, or a combination.

Second, what is the partner allowed to support under its own permissions? A partner may be licensed, but not necessarily for every function the fintech wants to build. The first version may fit, while the roadmap does not.

Third, who controls customer funds, balances, reconciliation, transaction records, data, complaints, AML/CFT operations, and customer communications? These details often matter more than the headline partnership.

Fourth, what will happen if the fintech outgrows the arrangement? The company should understand migration rights, exit rights, data portability, customer transition, and the operational process for moving to direct licensing or another partner.

Finally, how much dependency is acceptable at this stage? A market test can carry more dependency than a long-term regulated operating base. The structure should match the stage.

Conclusion

Sponsor dependency looks different in the UK and UAE because the two markets organise fintech regulation differently. The UK gives founders a clearer EMI path: agent, SEMI, AEMI. The UAE requires a more product-based analysis across retail payment services, stored value, open finance, payment tokens, agents, outsourcing, and licensed partner structures.

In both markets, sponsor dependency can be a smart way to launch faster. In both markets, it can become expensive when the business needs more control. The difference is that UK founders can usually describe the next step through the EMI ladder, while UAE founders need to map the next step against the exact regulated function of the product.

The best strategy is to treat sponsor dependency as a stage tool. Use it when it accelerates learning and reduces unnecessary early burden. Challenge it when it starts controlling the roadmap, economics, customer relationship, or regulated infrastructure the company needs to own. That discipline matters in every market, but it matters even more when expanding between the UK and the UAE, where similar commercial language can hide very different regulatory realities.