- Why UAE experience does not automatically define the UK route

- EMI agent: when the UK is still a validation market

- Where the EMI agent model becomes restrictive

- SEMI: when limited UK independence is enough

- When SEMI is not enough

- AEMI: when the UK becomes a strategic regulated market

- AEMI is not just a bigger licence

- How UAE starting points translate into UK choices

- The product questions UAE founders should ask first

- The dependency question

- Build the UK route as a staged plan

- Route selection

- Conclusion

A UAE fintech entering the UK should not treat the UK market as a simple extension of its existing regulatory setup. A product that works under a UAE partner-led model, Retail Payment Services licence, Stored Value Facilities structure, Open Finance route, or Payment Token Services framework still needs to be translated into the UK’s own payments and e-money map. The UK gives founders a clearer EMI-related sequence than the UAE, but that does not make the decision automatic.

The practical UK question is whether the company should launch through a principal EMI as an agent, register as a small electronic money institution, or pursue authorised EMI status. Each route represents a different balance between speed, independence, regulatory burden, governance maturity, and long-term control. For UAE fintechs, the right answer depends on what the product does, how much UK market uncertainty remains, and whether the company is entering the UK to validate demand or to build a regulated operating base.

At Finamp, we see this as a business-model decision first. The UK route should reflect the stage of the company, the maturity of its operations, the complexity of the product, and the level of regulated control the company needs in the UK. A UAE business should not choose AEMI because it sounds more mature, or SEMI because it sounds lighter. It should choose the route that matches the UK version of the product.

Why UAE experience does not automatically define the UK route

A UAE fintech may already understand regulated payments, customer onboarding, wallet operations, merchant flows, stored value, compliance controls, or partner-led launch models. That experience is valuable, but it does not remove the need for UK classification. The FCA requires firms to be authorised or registered if they want to provide payment services or issue electronic money in the UK. (FCA)

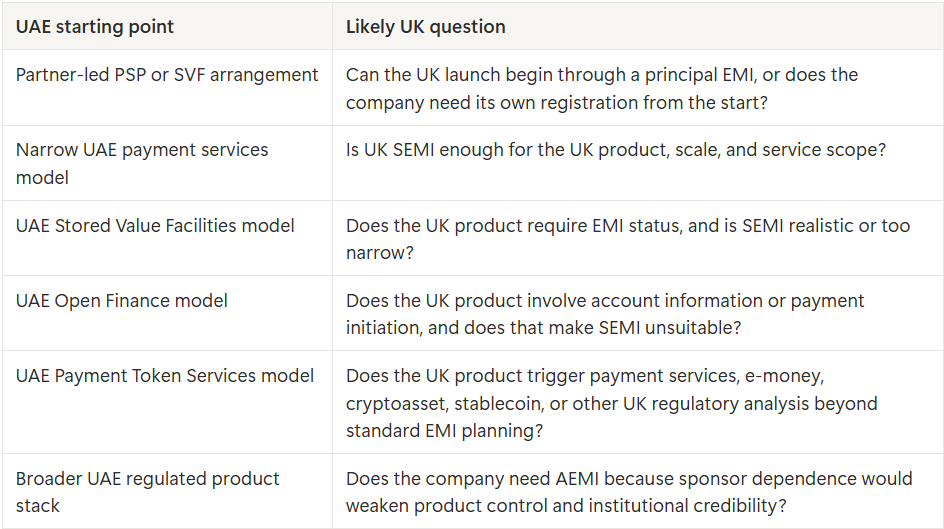

The reason this matters is that UAE product structures do not map directly to UK EMI labels. A UAE partner-led model may translate commercially into a UK EMI agent route. A UAE narrow payment services model may lead to a UK SEMI assessment if e-money issuance is involved and the product is limited enough. A UAE Stored Value Facilities product may push the company toward a more serious EMI analysis because the UK framework treats e-money issuance and safeguarding as core issues. A UAE Open Finance or Payment Token Services product may require additional UK analysis beyond the EMI question.

The starting point should therefore be a product translation exercise. The company should identify whether the UK product will issue e-money, provide payment services, hold customer funds, operate payment accounts, support transfers, provide account information, initiate payments, or use token-related settlement. Once that is clear, the EMI agent / SEMI / AEMI choice becomes much more practical.

EMI agent: when the UK is still a validation market

The EMI agent route usually makes sense when a UAE fintech wants to enter the UK without immediately becoming a regulated institution in its own name. In this model, the company operates through a principal EMI that carries the regulated permission and remains responsible for the agent’s acts and omissions. The FCA’s small EMI guidance explains that firms must register agents that provide EMI services on their behalf, and that the EMI is responsible for anything done or omitted by its agent and should have appropriate systems and controls to oversee them (FCA)

For a UAE fintech, this route can be especially useful when the UK is still a market-learning exercise. The company may know that its product works in the UAE, but the UK can still bring different onboarding expectations, customer acquisition costs, bank and partner requirements, payment habits, fraud patterns, complaint behaviour, and support needs. A principal EMI route can help the company test those conditions faster than building a direct UK regulatory setup from day one.

This is often the most practical route for UAE fintechs that already use partner-led structures at home. If the company is comfortable operating inside another regulated entity’s controls, reporting expectations, risk appetite, and approval process, the UK agent route may feel familiar at a business level. The legal structure is still UK-specific, but the commercial trade-off is similar: speed and reduced regulatory burden in exchange for dependency.

Where the EMI agent model becomes restrictive

The EMI agent model becomes less attractive when UK sponsor dependence starts shaping the product too heavily. A principal EMI will care about the company’s customer base, risk profile, onboarding logic, transaction flows, financial crime controls, complaints, and operational setup. That oversight is not incidental. It is part of why the model works.

For a UAE fintech with a simple UK market-entry proposition, this may be acceptable. For a company that already has a sophisticated regulated product in the UAE, the agent route can feel narrow. Product changes may require principal approval. New customer segments, transaction types, corridors, or pricing models may need to fit the principal’s risk appetite. The fintech may also face commercial costs through sponsor fees, revenue share, operational limits, and future migration work.

The route is therefore strongest when the company wants evidence before commitment. It becomes weaker when the UK product already requires direct control over the regulated layer. A UAE fintech should treat EMI agent as a launch structure, not as a substitute for a long-term UK operating model if the business expects serious scale or product complexity.

SEMI: when limited UK independence is enough

A small electronic money institution, or SEMI, can make sense when a UAE fintech wants its own UK regulatory status but does not yet need the full scope and burden of authorised EMI status. It is a middle route: more independent than operating as an agent, but narrower than AEMI.

The FCA small EMI guidance states that applicants must include details of their e-money business, governance arrangements, internal procedures, management, safeguarding approach, evidence that monthly average outstanding e-money will be less than €5 million, and evidence that monthly average payment services transactions did not exceed €3 million, or projections where the firm has not traded before. (FCA)

For UAE fintechs, SEMI is most useful when the UK product is clearly limited. The company may want to launch a focused UK wallet, a narrow stored-value proposition, a controlled payment feature, or a domestic use case that benefits from direct UK registration but does not require broad scale or open-ended product flexibility. SEMI can provide a clearer UK footprint than an agent model, while avoiding some of the weight of full authorisation.

This can be a smart move for a UAE fintech that already understands compliance operations and wants to avoid sponsor dependency, but still expects modest UK transaction volumes and a contained product roadmap. It can also support a founder who wants to build direct UK learning around safeguarding, governance, reporting, and customer operations before deciding whether AEMI is justified.

When SEMI is not enough

SEMI becomes the wrong choice when the UK roadmap is broader than the regime can support. The thresholds matter because they are operational constraints, not just legal details. A fintech that expects UK growth to move quickly beyond the €5 million average outstanding e-money limit or the €3 million monthly average payment transaction threshold may outgrow SEMI too early. (FCA)

There is also a product-scope issue. Small EMIs cannot provide account information services or payment initiation services. For UAE fintechs building around Open Finance, account data, service initiation, or embedded finance workflows, SEMI may not support the UK product direction. The company may need to assess other UK permission routes or move toward a broader authorisation strategy instead.

This is where UAE founders can overestimate SEMI’s usefulness. It sounds like a sensible middle step, and sometimes it is. But it should not be used as a placeholder for a product that already needs broader functionality, faster scale, or stronger institutional control. If the company knows from the beginning that UK growth will depend on services outside SEMI’s scope, the middle route may create rework rather than reduce burden.

AEMI: when the UK becomes a strategic regulated market

Authorised EMI status becomes relevant when the UAE fintech is not just testing the UK. It is choosing to build a UK regulated operating base. This route makes sense when the company needs direct control over the regulated layer, broader product flexibility, stronger partner credibility, more ownership of customer funds and safeguarding design, and the ability to run a more complex UK model.

The FCA’s electronic money and payment institutions page explains that firms need to be authorised or registered if they want to provide payment services or issue e-money, and it points firms toward requirements around conduct, safeguarding, policy, and authorisation. (FCA)

AEMI is often the stronger route when the UAE fintech already operates a mature regulated product at home. If the company runs wallet infrastructure, stored value, payment instruments, merchant payment flows, cross-border payments, or a broader regulated product stack, the UK version may require more control than an agent or SEMI structure can provide. AEMI can also become important when banks, enterprise clients, investors, or infrastructure partners expect direct UK regulatory substance.

The business case for AEMI becomes stronger when dependency is already known to be expensive. If the company has learned in the UAE that sponsor or partner limitations slow product development, compress margins, or complicate governance, it should be careful about recreating the same dependency in the UK unless the first launch is intentionally narrow.

AEMI is not just a bigger licence

AEMI should not be treated as a status upgrade for its own sake. It changes the company’s operating model. A firm pursuing authorised EMI status must be ready to carry direct responsibility for governance, controls, safeguarding, reporting, compliance, risk management, incident handling, customer operations, and regulated oversight.

That can be the right move, but only when the business case supports it. A UAE fintech entering the UK with a narrow, unproven product may not benefit from pushing full authorisation too early. It may spend too much time and capital before learning whether the UK market will support the proposition. But a UAE fintech with an already complex regulated product, serious UK partnerships, and a clear need for direct control may find that agent or SEMI routes are too restrictive from the beginning.

The useful test is simple: if the UK launch is mainly about learning, AEMI may be premature. If the UK launch is about building the company’s next regulated operating base, AEMI deserves early assessment.

How UAE starting points translate into UK choices

A UAE fintech can use its current operating model as a starting clue, but not as the final answer.

This translation should happen before the company chooses a UK entity setup, signs with a principal EMI, or starts an authorisation project. The UK route should follow from the product and business model, not from the company’s preferred label.

The product questions UAE founders should ask first

Before choosing EMI agent, SEMI, or AEMI, UAE founders should define the UK product in practical terms.

Does the product issue e-money or only facilitate payment flows? Does it maintain customer balances? Does it support payment accounts, payment instruments, merchant payments, domestic transfers, or cross-border transfers? Does it rely on account information or payment initiation? Does it involve token-based settlement or stablecoin-like value? Does the first UK version need full functionality, or can it launch as a narrower market test?

These questions matter because the UK route can change quickly once the product is described accurately. A simple payments feature may fit a partner-led launch. A limited UK wallet may support SEMI analysis. A broader financial account, payment instrument, and stored value product may point toward AEMI planning. An open finance-led product may require a different route from the start.

The dependency question

The next question is how much dependency the business can accept. EMI agent gives the fastest route but keeps the UAE fintech inside another institution’s approval process and risk appetite. SEMI reduces sponsor dependency but creates scale and service limits. AEMI gives the highest level of direct control but requires the strongest governance and operating readiness.

This is not only about compliance. It affects product velocity, pricing, customer experience, partner negotiations, reporting, migration risk, and investor perception. A UAE fintech entering the UK should therefore compare the total cost of each route, not only the application burden.

For early validation, dependency may be acceptable because the company is buying speed and learning. For long-term UK expansion, dependency may become a structural cost. The stronger the UK market signal becomes, the more important it is to know when the company would move from agent to SEMI, from SEMI to AEMI, or directly from partner-led launch to AEMI planning.

Build the UK route as a staged plan

The strongest UAE-to-UK strategies usually define a staged route rather than treating the first structure as permanent. A company may start as an EMI agent to test UK demand, prepare SEMI registration if the product is domestic and narrow, or begin AEMI planning in parallel if it already knows the UK product will need broader direct control.

The staging matters because a UK launch can succeed faster than the regulatory structure can adapt. If the company signs a sponsor arrangement without migration rights, data clarity, customer communication plans, operational continuity, or future licensing preparation, early success can create later friction. If the company pursues AEMI too early without enough market evidence, it may overcommit before the UK commercial case is proven.

A staged plan should identify the trigger points. Those triggers may include transaction volume, customer float, sponsor approval delays, margin compression, enterprise partner requirements, product expansion into new services, open finance needs, or the point where the company has enough UK operating evidence to justify direct authorisation.

Route selection

The EMI agent route usually makes sense when the UAE fintech wants speed, UK market validation, and a narrow first launch. It is strongest when the product can fit a principal EMI’s approved scope and when the company can accept sponsor dependency while it learns.

SEMI usually makes sense when the company wants its own UK registration, the product is UK-limited, transaction and e-money volumes are expected to remain modest, and the roadmap does not require AIS or PIS. It is strongest when the company needs more independence than an agent model but does not yet justify full AEMI.

AEMI usually makes sense when the UK is a strategic market, the product requires direct control over the regulated layer, the company expects meaningful scale or product complexity, and the team is ready to operate a stronger governance, safeguarding, risk, and compliance model. It is strongest when sponsor dependency would distort the economics or slow the product the company actually wants to build.

Conclusion

For UAE fintechs entering the UK, EMI agent, SEMI, and AEMI can be considered as three different answers to different stages of market entry.

EMI agent is usually the best fit when the company needs speed and UK market learning. SEMI can work when the company wants limited UK independence inside clear scale and service boundaries. AEMI becomes the right discussion when the UK is no longer just a test market and the company needs to own the regulated layer directly.

The best founders choose the UK route by looking at the product, the stage, the dependency they can accept, and the control they need next. A UAE fintech does not need to copy its home-market structure into the UK. It needs to translate the business model into the UK framework and choose the route that supports the next phase of growth.

Book a Call