Purpose

This discovery compares the UK fintech launch routes around EMI agent, SEMI, and AEMI with the closest available options in the UAE. The goal is to understand how the UAE market works in comparison with the UK, where the models are similar, where they differ, and how a fintech can think about transition between the two markets.

The main conclusion is clear: the UAE does not copy the UK EMI agent / SEMI / AEMI ladder directly. The UK model is easier to describe as a staged progression from sponsor dependency to limited independence and then full authorisation. The UAE requires a more product-based analysis across Retail Payment Services, Stored Value Facilities, Open Finance, Payment Token Services, and possible partner or agent arrangements with licensed entities.

This makes the UAE especially useful for a separate content cycle. Founders who understand the UK EMI landscape may still misunderstand the UAE if they try to search for direct equivalents. The better approach is to compare the business function of each route: speed to market, regulatory burden, product scope, dependency, capital requirements, and long-term control.

1. UK reference model

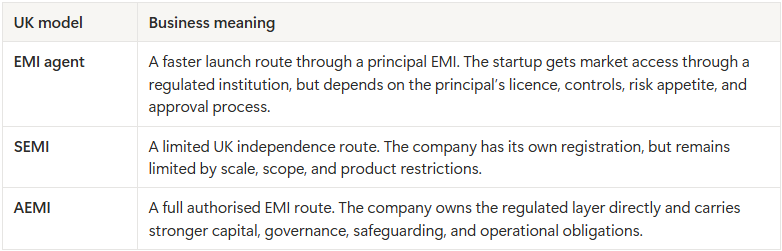

The UK structure can be explained through three main routes:

Under the FCA framework, EMIs may provide payment services through registered agents, and the principal accepts responsibility for the acts and omissions of the agent. Small EMIs are limited to average outstanding e-money not exceeding €5 million, cannot provide AIS or PIS, and must stay within the €3 million monthly average threshold for relevant unrelated payment services. Authorised EMIs carry broader governance, capital, safeguarding, and operational requirements. (FCA)

This creates a relatively clear UK progression:

EMI agent → SEMI → AEMI

However, this sequence should be understood as a business maturity path, not as a mandatory regulatory ladder. Some companies may stay with a sponsor model for longer. Others may move directly toward AEMI if their product, governance, and economics require it.

2. UAE regulatory landscape

The UAE uses a different structure. The most relevant frameworks are:

-

CBUAE Retail Payment Services and Card Schemes Regulation, or RPSCS Regulation

This covers digital retail payment services in the UAE. It includes nine categories of retail payment services, such as payment account issuance, payment instrument issuance, merchant acquiring, payment aggregation, domestic and cross-border fund transfers, payment token services, payment initiation, and payment account information services.

-

CBUAE Stored Value Facilities, or SVF, Regulation

This is the key framework for wallet-like or stored-value products where customer value is stored and later used for payments. The SVF route has materially heavier capital requirements, including paid-up capital of at least AED 15 million and aggregate capital funds of at least 5% of total customer float.

-

CBUAE Open Finance Regulation

This is relevant where the product involves data sharing, account information, or service initiation. The CBUAE describes Open Finance as a framework for the cross-sector sharing of data and initiation of transactions with user consent. (CBUAE)

-

CBUAE Payment Token Services Regulation

This becomes relevant if the product involves payment tokens, stablecoin-like functionality, or token-based settlement. The CBUAE rulebook states that no person may perform Payment Token Services within the UAE or directed to persons in the UAE unless licensed or registered by the Central Bank. (CBUAE Rulebook)

-

DIFC and ADGM financial free zone frameworks

DIFC and ADGM may be relevant for certain money services structures. ADGM’s FSRA has enhanced its Providing Money Services framework to cover payment accounts and stored value, and DFSA materials also refer to money services, stored value, and payment accounts. (ADGM)

However, free zone permissions should not be treated as a simple substitute for UAE mainland retail reach. For UAE onshore consumer payment activity, the CBUAE perimeter still needs to be assessed carefully.

3. UK vs UAE mapping

The RPSCS Regulation expressly allows a PSP to provide Retail Payment Services through agents or branches, but requires the PSP to assess the arrangement, report relevant information to the CBUAE annually, ensure agents disclose they act on the PSP’s behalf, and notify the Central Bank of changes. For SVF licensees, the regulation states that the licensee is responsible for the acts or omissions of employees, service providers, and agents.

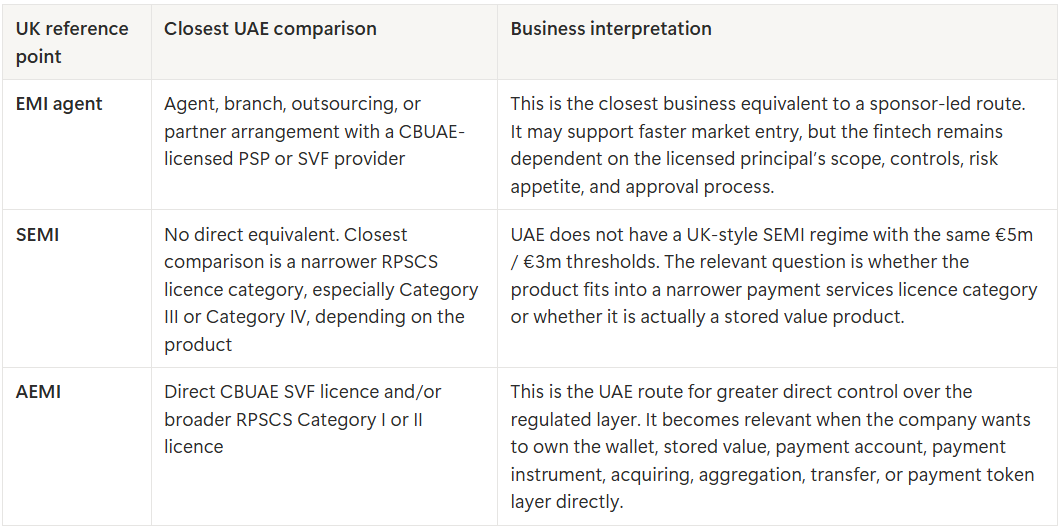

This means that the UAE can support sponsor-like or partner-led operating models, but they should not be described as a direct copy of the UK EMI agent model.

4. What replaces the SEMI logic in the UAE?

The UK SEMI model creates confusion because founders often search for a UAE equivalent. There is no exact equivalent.

In the UAE, the more useful comparison is between:

- a partner-led route through a licensed PSP or SVF provider;

- a narrower RPSCS licence for limited payment services;

- a fuller RPSCS licence for broader payment services;

- an SVF licence for stored value or wallet products.

The RPSCS Regulation has four licence categories. Category I is the broadest and includes services such as payment account issuance, payment instrument issuance, merchant acquiring, payment aggregation, domestic and cross-border fund transfers, and payment token services. Category II covers a broad set of services but excludes payment token services. Category III covers a narrower group of retail payment services. Category IV covers payment initiation and payment account information services.

Capital also works differently from the UK SEMI model. Under the RPSCS Regulation, initial capital depends on the category and whether the monthly average value of payment transactions is below or above AED 10 million. For example, Category I requires AED 3 million if monthly average transaction value is AED 10 million or above, or AED 1.5 million below that level. Category III requires AED 1 million above the AED 10 million threshold, or AED 500,000 below it. Category IV requires AED 100,000 regardless of monthly average transaction value.

For stored value products, the capital burden is much higher. SVF licensees must maintain paid-up capital of at least AED 15 million and aggregate capital funds of at least 5% of total float received from customers.

This is the key discovery point: in the UK, SEMI is a small e-money route. In the UAE, a founder must first identify whether the product is a payment service, stored value facility, open finance service, payment token service, or a combination of these.

5. UK fintech entering the UAE

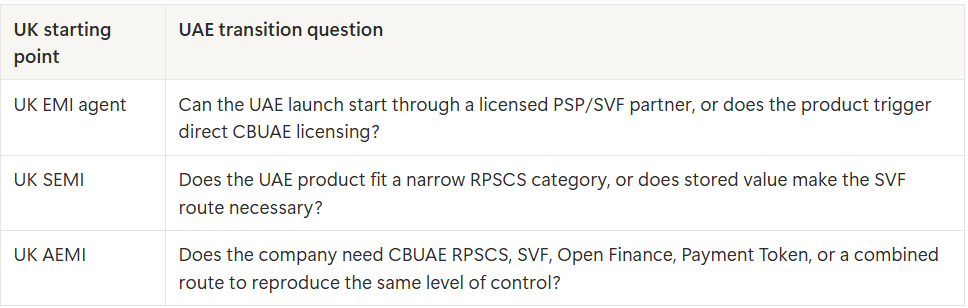

A UK fintech entering the UAE should not start by asking, “What is the UAE version of EMI agent, SEMI, or AEMI?” That framing can lead to wrong assumptions. The better starting point is product classification.

The first question is whether the product stores customer value or only moves funds in transit. If the product behaves like a wallet, stored balance, prepaid value, or customer float model, the SVF framework may become central. If the product provides payment account issuance, card or instrument issuance, acquiring, aggregation, domestic transfers, cross-border transfers, payment initiation, or account information, the RPSCS categories become relevant. The RPSCS Regulation also excludes payment transactions involving Stored Value Facilities from its scope, which makes the boundary between RPSCS and SVF especially important.

The second question is whether the company can launch through a licensed UAE partner first. This may be the closest business comparison to the UK EMI agent or sponsor route. It can support faster market entry, but it creates dependence on the licensed entity’s regulatory scope, risk appetite, onboarding rules, monitoring controls, and commercial terms. This route may be appropriate for early market validation, especially where the company is still testing product-market fit, user behaviour, transaction flows, or distribution channels.

The third question is whether direct licensing is already needed. If the product requires direct control over wallet balances, customer funds, payment accounts, instruments, token services, or more complex regulated functionality, the company may need to assess direct CBUAE licensing earlier. This is where UAE market entry becomes more demanding than a simple sponsor-led commercial expansion.

For UK founders, the practical transition logic is:

6. UAE fintech entering the UK

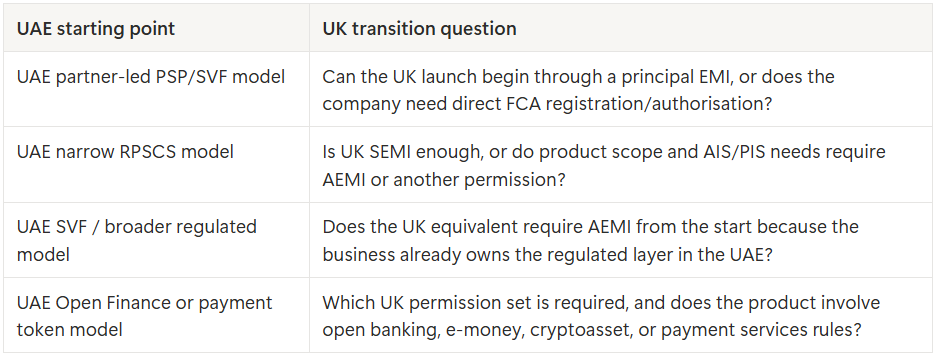

For a UAE fintech entering the UK, the comparison works in the opposite direction. The UK has a clearer set of EMI-related routes, but each route imposes different trade-offs.

A UAE fintech that wants to test the UK market may start with a principal EMI or sponsor-style arrangement. This may be useful if the company wants market access before building full FCA-regulated operations. The trade-off is dependence, because the principal remains central to compliance, controls, and risk appetite.

A UAE fintech that wants its own UK regulatory status but expects limited domestic scale may assess SEMI. This route can be useful only where the product fits the limits: average outstanding e-money must not exceed €5 million, relevant unrelated payment transactions must not exceed the €3 million monthly average threshold, and the firm cannot provide AIS or PIS. (FCA)

A UAE fintech that needs broader UK control, more complex payment functionality, or stronger institutional positioning may need to assess AEMI. That route is more demanding because the company must carry direct governance, safeguarding, capital, and operational responsibilities.

For UAE founders, the practical transition logic is:

7. Business implications for founders

The UK and UAE comparison should be framed around business decisions, not only regulatory names.

The first decision is speed versus control. In both markets, partner-led arrangements can support faster entry, but dependence becomes more expensive as the product grows. The difference is that the UK sponsor model is easier to explain through EMI agent logic, while the UAE requires a more specific assessment of PSP, SVF, agent, outsourcing, and partner arrangements.

The second decision is payment service versus stored value. This distinction is especially important in the UAE because stored value may move the product into the SVF framework, which has much heavier capital and float-related requirements than narrower RPSCS categories.

The third decision is local validation versus regional or cross-border ambition. A UK SEMI can make sense for a UK-limited product, but it is not a passporting tool. A UAE RPSCS or SVF route may support a UAE product, but it does not automatically answer how the company enters the UK. Each direction requires a separate market-entry map.

The fourth decision is product complexity. If the product includes payment initiation, account information, open finance data sharing, stored value, payment tokens, or cross-border transfers, the route becomes more complex. In the UAE, these areas may fall under different parts of the CBUAE framework, including RPSCS, Open Finance, SVF, or Payment Token Services.

8. Discovery checklist

Before writing UAE-focused articles or advising on a UK ↔ UAE transition story, the following questions should be answered for each product:

- Does the product issue or store customer value?

- Does the product only move funds, or does it maintain balances?

- Does it involve payment accounts or payment instruments?

- Does it include domestic transfers, cross-border transfers, merchant acquiring, or payment aggregation?

- Does it involve account information or payment initiation?

- Does it involve Open Finance data sharing or service initiation?

- Does it involve payment tokens or stablecoin-like settlement?

- Can the first launch happen through a licensed partner?

- If a partner is used, which regulated entity remains responsible for customer funds, controls, AML/CFT, reporting, and complaint handling?

- Does the business need direct control now, or is market validation still the priority?

- What is the likely transaction volume and customer float over the first 12-24 months?

- Does the product roadmap require expansion from the UK to UAE, UAE to UK, or both?

9. Useful sources

- FCA Payment Services and Electronic Money Approach Document, for the UK EMI agent, SEMI, and AEMI reference model. (FCA)

- CBUAE Retail Payment Services and Card Schemes Regulation, for UAE retail payment service categories, licence categories, capital requirements, and agent/branch rules. (RPSCS Regulation)

- CBUAE Stored Value Facilities Regulation, for wallet and stored value requirements, including paid-up capital and float-based capital funds. (SVF Regulation)

- CBUAE Open Finance Regulation materials, for data sharing and service initiation in the UAE. (CBUAE)

- CBUAE Payment Token Services Regulation, for payment token and stablecoin-like product analysis. (CBUAE Rulebook)

- ADGM and DFSA materials on Providing Money Services, for free zone context. (ADGM)